doi: 10.58763/rc2026553

Scientific and technological research article

Ética del contador público en el ejercicio de la docencia universitaria

Ethics of public accountants in university teaching

Olga

Calizaya Pari 1 ![]() *, Nicohl

Brenda Quispe Mamani 1

*, Nicohl

Brenda Quispe Mamani 1 ![]() *, Rafael

Romero-Carazas1

*, Rafael

Romero-Carazas1 ![]() *

*

RESUMEN

Introducción: El presente artículo tiene el objetivo de explorar cómo los contadores públicos que ejercen la docencia universitaria aplican y gestionan los principios éticos en la práctica educativa.

Metodología: La metodología aplicada es de enfoque cualitativo, método inductivo, diseño fenomenológico y con alcance descriptivo. Para este artículo se consideró como muestra a docentes universitarios de la carrera de Contabilidad; se utilizó como técnica e instrumento la entrevista.

Resultados y Discusión: Como resultado, se obtuvo que los docentes se enfrentan a diferentes desafíos y dilemas éticos, como la modificación de notas de estudiantes, el enfrentar cambios normativos, puesto que deberán estar actualizados, y las estrategias pedagógicas que deberán utilizar al enseñar a sus estudiantes de acuerdo al temario del curso y relacionándolo con la ética.

Conclusiones: En conclusión, la ética es percibida como conjunto de valores que deben ser transmitidos con conocimientos técnicos, práctica y ejemplo a estudiantes de la carrera, puesto que es esencial para mantener la confianza pública y la integridad del sistema económico.

Palabras clave: Ética; contabilidad; valores morales; docencia; universidad.

Clasificación JEL: M40, M39.

ABSTRACT

Introduction: The aim of this article is to explore how public accountants who teach at the university level apply and manage ethical principles in their educational practice.

Methodology: The methodology applied is qualitative, using an inductive method, a phenomenological design, and a descriptive scope. For this article, the sample consisted of university professors from the Accounting program; the interview was used as the technique and instrument.

Results and Discussion: The results showed that the professors face various ethical challenges and dilemmas, such as modifying student grades, adapting to regulatory changes (which require them to stay up-to-date), and developing pedagogical strategies to teach their students effectively, aligning the course content with ethical considerations.

Conclusions: In conclusion, ethics is perceived as a set of values that must be transmitted to accounting students through technical knowledge, practical application, and exemplary behavior, as it is essential for maintaining public trust and the integrity of the economic system.

Keywords: Ethics; accounting; moral values; teaching; university.

JEL Classification: M40, M39.

Received: 16-08-2026 Revised: 22-11-2026 Accepted: 15-12-2025 Published: 02-01-2026

Editor:

Alfredo Javier Pérez Gamboa ![]()

1Universidad Tecnológica del Perú. Arequipa, Perú.

Cite as: Calizaya Pari, O., Quispe Mamani, N. B., & Romero-Carazas, R. (2026). Ética del contador público en el ejercicio de la docencia universitaria. Región Científica, 5(1), 2026553. https://doi.org/10.58763/rc2026553

INTRODUCTION

In a highly competitive business environment, numerous accountants find themselves in situations where they must choose between preserving their professional ethics and meeting the expectations of their employers or clients. These expectations may sometimes involve questionable actions such as altering financial statements, engaging in covert tax evasion, or deliberately concealing relevant information. However, accounting professionals have a duty to always behave and act in the best interest of the public. Therefore, this study focuses on the ethics of public accountants in the context of university teaching.

Ethics in a person is crucial for guiding individuals in social life, since personal and societal conduct is evaluated in different contexts, allowing individuals to make decisions that promote harmony with the environment in which they develop (Zeledón Ruiz & Aguilar Rojas, 2020). Quilia Valerio et al. (2023) point out that accounting professionals find themselves in a complicated situation due to scandals linked to the unethical conduct of public accountants acting for their own benefit. Considering the activities that public accountants carry out in their companies and the unconditional trust of their clients, this study examines how they manifest and manage ethical principles in their practice as university professors to adequately fulfill their professional responsibilities.

The research on the ethics of public accountants in university teaching stems from previous studies that have observed and corroborated that ethics should be considered important in universities and other circumstances or contexts, but it is not fully applied. For example, research at the University of Panama has shown that ethics is the moral compass of the public accountant and has an impact on higher education institutions such as universities, institutes, and faculties, among others. It is important to implement ethics in the professional field of accounting to improve the quality of work of each professional, whether in the public sector or in private companies. All work must be carried out in accordance with the principles of the professional code of ethics. Compliance with this code ensures that information is transparent, reliable, and trustworthy for society. For this reason, this article is based on various theoretical approaches related to ethics, professional ethics, the epistemology of ethics, and the ethical dimensions inherent in accounting practice. First, ethics is conceived as a branch of philosophy responsible for analyzing and evaluating human behavior, particularly its relationship to the concepts of good and evil. Mendieta (2022) maintains that ethics fulfills this evaluative function of human actions, while Castellanos Polo et al. (2023) emphasize its close relationship with morality, as both guide individual conduct and decisions within a society.

From a more specific perspective, professional ethics is understood as the set of principles, values, and action frameworks that guide the professional’s conduct in their field of work. Moreno Aguirre and Báez Sepúlveda (2023) affirm that these elements are fundamental for a responsible and efficient practice of the profession. Along these lines, Bani Ahmad (2024) argues that professional ethics constitutes an extension of philosophical ethics, whose function is to guide human actions and promote appropriate decisions within the workplace.

Regarding the epistemology of ethics, the conceptual origin of the term is addressed. Avendaño Calderón (2022) indicates that “ethics” comes from the Greek word ἦθος (ethos), which means “custom.” However, Vergara Castillo et al. (2021) complement this notion by pointing out that the term also derives from ethikos, which translates as “character.” This etymological duality allows us to understand ethics both as a socially constructed habit and as an expression of individual character.

When addressing the ethical dimensions in the accounting profession, it is recognized that this discipline encompasses various functions, including financial accounting, tax consulting, management accounting, and financial analysis. According to Cruz-Pérez and Cordero-Díaz (2022), the ethical practice of the profession involves preparing reports in a truthful and transparent manner, which significantly contributes to strengthening public trust and achieving organizational goals.

Within this framework, ethical principles play an essential role in regulating the behavior of the public accountant. Ruiz Pardo (2021) identifies several fundamental principles that guide professional practice. These include the principle of integrity, which demands acting with honesty, dignity, and sincerity. Likewise, the principle of objectivity requires impartiality in professional judgment and the avoidance of biases or favoritism.

Furthermore, the principle of independence establishes the need to make decisions free from external influences, maintaining professional transparency. The principle of competence implies the constant updating of knowledge, regulations, and technical skills to guarantee effective performance. Finally, the principle of confidentiality requires the protection of information obtained during professional practice, preventing its disclosure to third parties without the corresponding consent.

Therefore, values are understood as moral references that guide individual and professional conduct. Moreno Aguirre and Báez Sepúlveda (2023) affirm that values are closely linked to morality and ethical principles, and that they are transmitted intergenerationally as a guide for the common good. Along the same lines, Sepulveda Covarrubias (2023) defines them as beliefs and behaviors that tend towards good, and that allow distinguishing between what is permitted and what is not permitted within the ethical-social framework.

Additionally, in previous studies, Quilia Valerio et al. (2023) noted that one of the primary objectives of accountants and related entities in the field of accounting is to eradicate the distrust generated by professionals with low moral standards and to safeguard their professional prestige so that it is not weakened by public opinion. Likewise, the ethics of accountants can sometimes be affected by the private or public entities for which they work, with the aim of compromising their role as public trustees through events and influences. For this reason, according to Pinzón Alfonso and Serrato Guana (2021), they indicated that social responsibility rests not only with the accountant, but also with the companies and the social context.

For this reason, Agudelo Vargas et al. (2022) indicated that the individual who performs the role of public accountant has the obligation to act for the benefit of the public, without prioritizing their personal interests or those of related third parties. Unfortunately, in this society, there have been acts of fraud, alteration of accounting information, and unethical behaviors that affect the credibility of the profession and the integrity of those who practice it.

Regarding Changmarín R. and Vargas de Changmarín (2021), they anticipated that public accountants who lack training in ethical standards will see their credibility diminish over time, as they argue that codes of ethics lack a permanent updating program. The findings indicate that currently, no more than 50 % of national accounting institutions implement the code of ethics in accounting practice. It is also argued that the International Ethics Standards Board for Accountants (IESBA) plays an essential role in strengthening the reputation of public accountants and the companies they represent.

In the vast majority of professionals, there is a failure to comply with these codes of ethics, since each individual independently decides whether or not to comply, as they are also influenced by public entities and companies where they work to satisfy their own needs and those of taxpayers, for example, paying less in taxes (Pirela Espina, 2022). This paper highlights several crucial factors that demonstrate the tensions, challenges, and perspectives that professors face when teaching ethics to future accountants. In this context, Romero-Carazas et al. (2024) determined that most accountants in Peru act unethically; these behaviors contribute to the increase in corruption in the country, normalizing the current crisis of values and thus perpetuating unethical behaviors and actions. In this context, public accountants have an obligation to act with responsibility, respect, honesty, and fairness, both in their accounting work in different areas and in their daily lives.

The Code of Ethics for public accountants in Peru was established by the Board of Deans of the Colleges of Public Accountants of Peru, with contributions from departmental public accountants. According to Article 1 of Supreme Decree No. 008-93-JUS, the purpose of this code of ethics is to define rules that regulate the behavior of certified public accountants. This code defined the basic principles, the performance of the accounting profession, interactions with other colleagues and third parties, the accountant’s responsibility, the disciplinary system, and the disciplinary authorities.

Amidst a growing need for professional education grounded in values and social responsibility, it is crucial to examine the role of public accountants who, in addition to practicing their profession, also serve as university professors. These experts not only impart technical knowledge but also play an educational role in the ethical formation of future accountants. Therefore, the main objective of this research was to explore how public accountants who teach at the university level apply and manage ethical principles in their educational practice, understanding that their impact transcends the classroom, shaping attitudes and moral norms in future generations.

METHODOLOGY

This study employs a qualitative approach and a descriptive scope. Non-numerical data were collected and analyzed to understand social phenomena, based on the collection of opinions, behaviors, and other lived experiences of each teacher (Molano De La Roche et al., 2021). According to Calle Mollo (2023), the phenomenological design studies phenomena from the perspective of each subject, seeking to discern the meanings and responses of each person, describing the experience and explaining the reasons for their actions. Based on the above, the design of this research is phenomenological, as it aims to obtain the different responses of each university professor. The descriptive scope is due to the representation of the different characteristics of each professor and the exploration of their ideas on the definitions of ethics. Furthermore, Alegre Brítez (2022) points out that the descriptive level specifies the characteristics of individuals and groups, providing information for subsequent analysis.

The population of this study consisted of university professors in the accounting program at universities in the Arequipa region during 2025, considering that the population is a set of subjects or objects to be investigated (Lim, 2025). In this research, the sample consisted of a total of nine university professors from the accounting program at universities such as (2) Universidad Tecnológica del Perú, (3) Universidad Nacional de San Agustín, (2) Universidad Católica de Santa María, and (2) Universidad Católica San Pablo. In qualitative research, the sample refers to a group selected intentionally and non-probabilistically, chosen to gain a deep understanding of a specific phenomenon (Hernández-Sampieri & Mendoza, 2020).

The analysis of the acquired information was qualitative and interpretive, complemented by theoretical references and the application of a semi-structured interview with four questions, which was used as a technique for this study, along with the use of Atlas.ti software. The Atlas.ti tool allowed us to analyze and interpret information from qualitative research (Cipollone, 2022). Finally, the research lasted five months, during which all stages of the study were carried out, from initial planning to data collection and analysis. During this time, the aforementioned techniques and methodologies were implemented to ensure the validity and reliability of the results, allowing for the collection of information that guaranteed a comprehensive understanding of the phenomenon under investigation.

Prior Selection of Codes

To guide the qualitative research, a prior selection of codes was defined, focusing on the conceptual variable of ethics, understood as the study of human behavior guided by principles. This coding was organized around the category of ethical principles in the teaching practice of certified public accountants and was broken down into key subcategories. The instrument used was the interview, which allowed for the structuring and in-depth exploration of the ethical aspects linked to teaching practice.

|

Table 1. Prior selection of codes |

||||

|

Conceptual Variables |

Definition |

Category |

Subcategory |

Instrument |

|

Ethics |

Ethics is the discipline that analyzes human behavior and defends the principles that guide it. |

Ethical principles in the teaching practice of certified public accountants. |

Ethical perceptions Ethical principles Ethical challenges Professional training and experience |

Interview |

RESULTS

Qualitative, phenomenological hermeneutic analysis

|

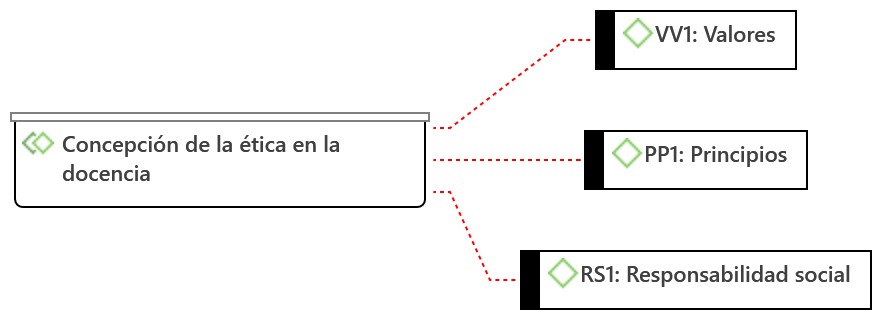

Figure 1. Network of codes from the first interaction. |

|

|

|

Note: The figure is in its original language. |

Regarding the first question, university professors associate ethics with a set of values such as honesty, social responsibility, and respect, referring to the fundamental principles that should guide teaching and practice. They also point out that ethics is not merely academic knowledge, but must be exemplified and demonstrated for students.

|

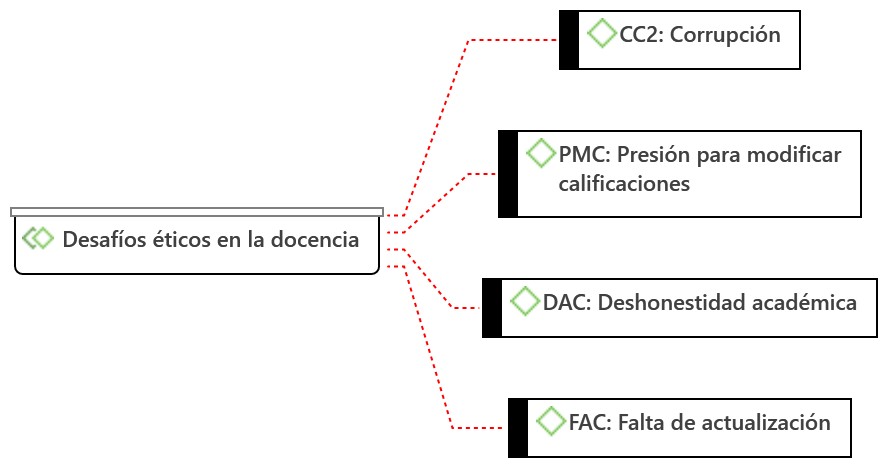

Figure 2. Code network of the second interaction |

|

|

|

Note: The figure is in its original language. |

Regarding the second interview question, it addressed the various challenges faced by educators. One of the main problems highlighted was the need to update regulations in accordance with professional development, such as the International Financial Reporting Standards (IFRS). Another challenge mentioned was the impact of technological advancements on performance and training requirements. Furthermore, educators face pressure to maintain their integrity in the face of situations such as corruption or fraud, for example, when they are pressured to alter grades or ignore dishonest behavior.

|

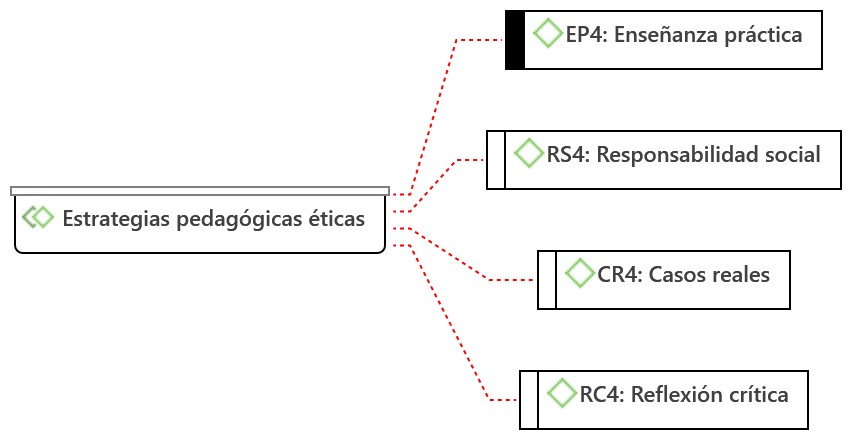

Figure 3. Code network of the third interaction |

|

|

|

Note: The figure is in its original language. |

In the third question, various pedagogical strategies were observed. Based on this observation, it is necessary to incorporate more practical case studies into accounting education because ethical principles should not only be understood but also put into practice. Furthermore, ethical training requires practical application, continuous discussions, and the exploration of ethical dilemmas, among other approaches.

|

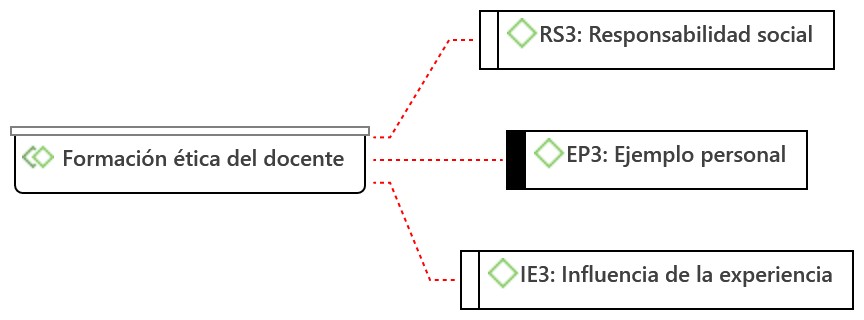

Figure 4. Code network of the fourth interaction |

|

|

|

Note: The figure is in its original language. |

In this case, it means that the teacher must reflect ethical principles in their daily life because students learn not only from what they are taught, but also by observing how teachers confront and resolve ethical dilemmas that arise in their daily practice.

|

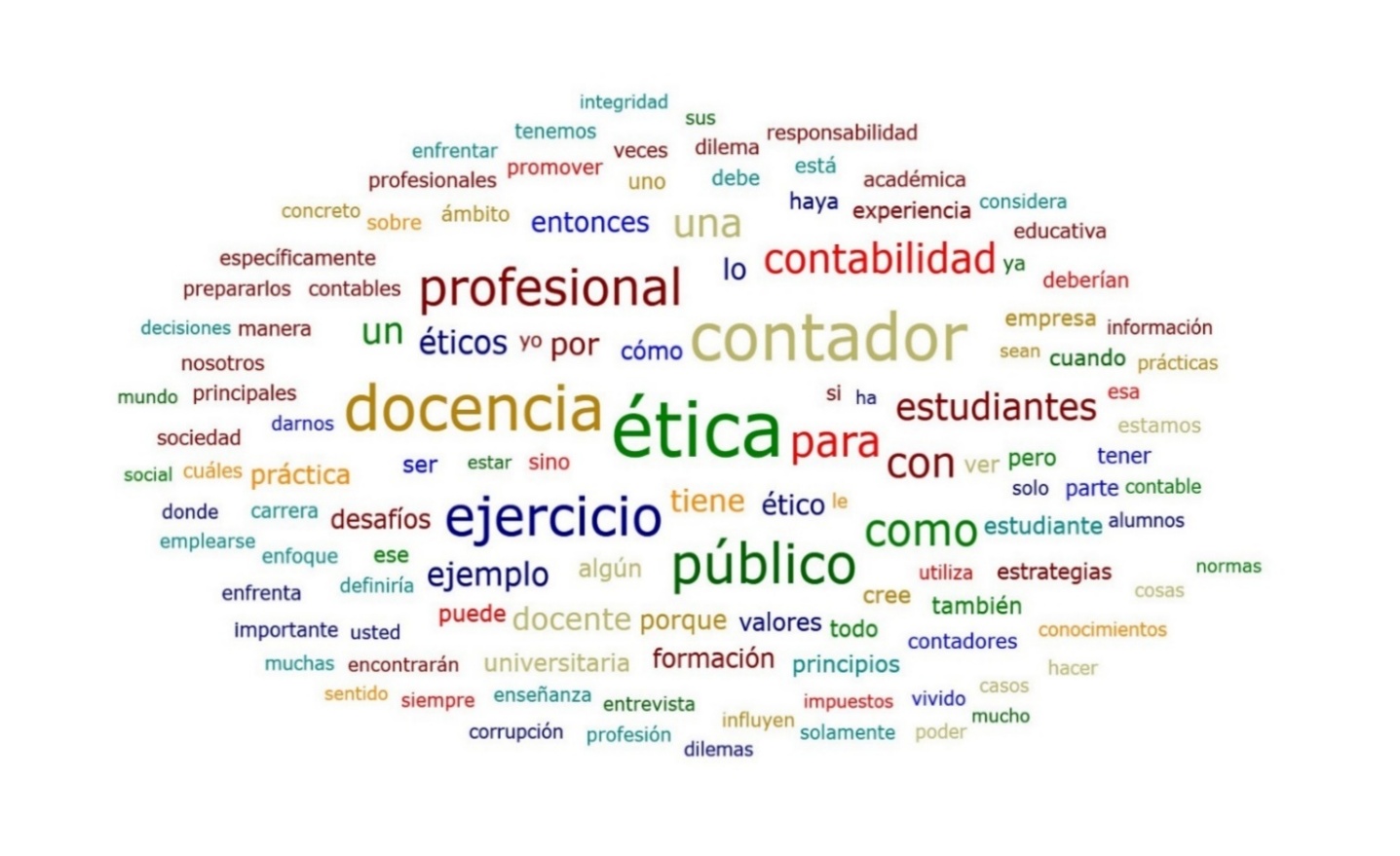

Figure 5. Word cloud of the interactions |

|

|

|

Note: The figure is in its original language. |

The word cloud highlights the essential elements of ethical teaching in university accounting programs, emphasizing the importance of teaching ethics through examples and practical application, not just theoretical knowledge. Students need to be taught values such as honesty, social responsibility, and integrity. Ethical challenges, such as academic dishonesty, pressure to alter grades, and corruption, are recurring issues. Therefore, educators must confront these situations in their daily practice. Finally, teachers must serve as role models, setting a positive example and dynamically conveying these values in their work as educators.

DISCUSSION

Ethics as a set of fundamental values

Professional ethics must be linked to the professional’s internal values, as they must act with respect and autonomy. Similarly, the interview results reflected that the teacher should not only teach ethical principles theoretically, but also demonstrate them through their behavior and values (interview 2). This result aligns with Soto Abanto et al. (2022), who state that the teacher must be a role model, since students learn not only through theoretical instruction but also by observing the teacher’s ethical behavior.

Ethical challenges in accounting education

One of the most significant challenges identified is the lack of updated technological tools and the constant changes in regulations, such as IFRS. Changmarín R. and Vargas de Changmarín (2021) report that the lack of continuing education programs is an obstacle to ethical accounting practices. Interviews also revealed that instructors are facing ethical dilemmas when teaching outdated standards; this can raise concerns about the quality of ethical and professional training.

The disconnect between theory and practice

In the interviews conducted, teachers indicated that it is necessary to use more practical case studies and real-world ethical dilemmas in the classroom (interview 3). Martínez De León and Serracín Conte (2024) corroborate that student are disconnected from reality; therefore, they are unaware of ethical principles because they do not have a course on ethical principles within their study programs.

Strategies to promote professional ethics

Teachers suggest incorporating more case studies, simulations, and social responsibility projects (interview 5). Pirela Espina (2022) also indicates that students should possess the ability to handle situations where they must decide between ethical and unethical actions, and what is beneficial for the organization. Changmarín R. and Vargas de Changmarín (2021) affirm that public accountants who do not receive training in ethics may lose credibility in the long run. This finding suggests that universities and instructors should not only teach accounting topics but also prioritize the values and ethical principles of accountants.

The example as a teaching strategy

Another key strategy that was identified is the example that a teacher can set for their students. Bedoya-Parra et al. (2021) affirm that ethics are not only taught in the classroom, but also demonstrated in the teacher’s daily behavior and how they address unethical issues during their professional practice. In the interview, the teachers indicated that students learn more from what they observe than from the theory they hear (interview 2, 7). Furthermore, Quilla et al. (2023) point out that teachers should act as role models to promote an ethical culture, as students will imitate them in their professional practice.

CONCLUSIONS

Through a descriptive analysis of the ethics variable, it is concluded that ethics is perceived as a set of fundamental values that should be taught not only through theoretical knowledge but also through practice and example. It is determined that teachers face several significant challenges, such as pressure to alter grades, academic dishonesty, and a lack of professional development, both in regulatory matters and technological advancements.

The ethical pedagogical strategies highlighted include practical case studies, critical reflection, and instruction through examples, considering social and professional responsibility in the training of future accountants. The hermeneutic analysis indicates that professional ethics in university accounting education is a multidimensional issue, encompassing core values and the challenges of incorporating them into an ever-changing educational landscape. It is important for teachers to address the topic of ethics in their courses, not only theoretically but also practically, as accountants must serve the public interest, both in their professional roles within organizations and, even more so, in their role as educators and mentors of future professionals.

REFERENCES

Agudelo Vargas, M. V., Chirinos Araque, Y. del V. & Viloria Ortega, N. J. (2022). Ética de la autenticidad y ejercicio profesional del contador público. Revista Venezolana de Gerencia, 27(99), 1196-1214. https://doi.org/10.52080/rvgluz.27.99.22

Alegre Brítez, M. Á. (2022). Aspectos relevantes en las técnicas e instrumentos de recolección de datos en la investigación cualitativa. Una reflexión conceptual. Población y desarrollo, 28(54), 93–100. https://scielo.iics.una.py/scielo.php?script=sci_arttext&pid=S2076-054X2022005400093

Avendaño Calderón, O. de J. (2022). El Código Internacional de Ética Profesional para Contadores Públicos. Una reflexión sobre la complejidad en su aplicación. Revista Colombiana de Contabilidad, 10(19), 1-27. https://doi.org/10.56241/asf.v10n19.229

Bani Ahmad, A. (2024). Ethical implications of artificial intelligence in accounting: A framework for responsible ai adoption in multinational corporations in Jordan. International Journal of Data and Network Science, 8(1), 401–414. https://doi.org/10.5267/j.ijdns.2023.9.014

Bedoya-Parra, L., Sánchez-Mayorga, X., & Sánchez-Cabrera, S. A. (2021). Ética y responsabilidad social como mecanismos de formación integral para el ejercicio profesional del Contador. Entramado, 17(2), 146–161. https://doi.org/10.18041/1900-3803/entramado.2.7829

Calle Mollo, S. E. (2023). Diseños de investigación cualitativa y cuantitativa. Ciencia Latina Revista Científica Multidisciplinar, 7(4), 1865–1879. https://doi.org/10.37811/cl_rcm.v7i4.7016

Castellanos Polo, O. C., Murillo Mosquera, D. A., Ricardo López, M. A., & Caballero Correa, M. A. (2023). La Importancia de la ética Profesional en la Auditoría Financiera. REVISTA PENSAMIENTO TRANSFORMACIONAL, 2(5), 48–65. https://doi.org/10.63526/pt.v2i5.37

Changmarín R., C. A., & Vargas de Changmarín, M. (2021). Prospectiva de los Códigos de Ética, su aplicabilidad y la docencia de la ética en el ejercicio profesional, en la profesión de la contabilidad. Societas, 23(1), 50-71. https://doi.org/10.48204/j.societas.v23n1a3

Cipollone, M. D. (2022). Atlas.ti como recurso metodológico en investigación educativa. Anuario Digital De Investigación Educativa, 5. https://revistas.bibdigital.uccor.edu.ar/index.php/adiv/article/view/5280

Cruz-Pérez, O. A., & Cordero-Díaz, M. C. (2022). Formación ética del contador público en instituciones de educación superior en Colombia. Reflexiones Contables, 5(1), 57-69. https://doi.org/10.22463/26655543.3598

Hernández-Sampieri, R., & Mendoza, C. (2020). Metodología de la investigación. Las rutas cuantitativa, cualitativa y mixta Las rutas Cuantitativa Cualitativa y Mixta. In McGRAW-HILL Interamericana Editores S.A. de C.V

Lim, W. M. (2025). What Is Qualitative Research? An Overview and Guidelines. Australasian Marketing Journal, 33(2), 199–229. https://journals.sagepub.com/doi/10.1177/14413582241264619

Martínez De León, V. I., & Serracín Conte, A. E. (2024). Formación Ética del Contador en la Facultad de Administración de Empresas y Contabilidad, Universidad de Panamá. CPA Panamá, 2(1), 70-89. https://doi.org/10.48204/2953-3147.4709

Mendieta, L. (2022). Ética y moral del docente universitario. Una interpretación a Kant. Ciencia y Desarrollo, 25(1), 99-109. https://doi.org/10.21503/cyd.v25i1.2358

Molano De La Roche, M., Valencia Estupiñán, A. M., & Apraez Pulido M. A. (2021). Características e importancia de la metodología cualitativa en la investigación científica. Semillas del Saber,1(1). https://revistas.unicatolica.edu.co/revista/index.php/semillas/article/view/314

Moreno Aguirre, J., & Báez Sepúlveda, M. (2023). Ética Profesional, Disidencia e Incidencia en la Formación Docente Contemporánea. Revista Docencia Universitaria, 25(1), 1-17. https://doi.org/10.18273/revdu.v25n1-2024001

Pinzón Alfonso, R. H., & Serrato Guana, A. D. (2021). El dilema ético del contador público en Colombia. Una reflexión sobre su función social de garantizar la confianza pública. Cuadernos de Contabilidad, 22, 1–10. https://doi.org/10.11144/javeriana.cc22.decp

Pirela Espina, W. A. (2022). Influence of university education on the formation of the tax culture of the public accountant. Visión de Futuro, 26(1), 22-37. https://doi.org/10.36995/j.visiondefuturo.2021.26.01.001.en

Quilia Valerio, J. V. M., Rimache Inca, M. & Alfaro Mendoza, J. A. (2023). La Ética Profesional en la formación y en el ejercicio profesional del Contador Público. Revista de Filosofía y Ciencias, (27), 88-99. https://doi.org/10.34024/prometeica.2023.27.14874

Romero-Carazas, R., Chávez-Díaz, J. M., Ochoa-Tataje, F. A., Segovia-Abarca, E., Monterroso-Unuysuncco, I., Ocupa Julca, N., Chávez-Choque, M. E., & Bernedo-Moreira, D. H. (2024). The Ethics of the Public Accountant: A Phenomenological Study. Academic Journal of Interdisciplinary Studies, 13(1), 339. https://doi.org/10.36941/ajis-2024-0025

Ruiz Pardo, R. (2021). Principio de Ética; confidencialidad en la profesión contable. Pensamiento Republicano, (13), 89-99. https://doi.org/10.21017/Pen.Repub.2021.n13.a77

Sepulveda Covarrubias, M. (2023). Conocimiento y práctica de valores éticos y morales en tres escuelas primarias en las zonas conurbadas de Chilpancingo Guerrero. LATAM Revista Latinoamericana de Ciencias Sociales y Humanidades, 4(1), 54–69. https://doi.org/10.56712/latam.v4i1.223

Soto Abanto, S. E., Martin Vergara, J. A., Alvarado Espinoza, J. O., & Guarniz Benites, O. C. (2022). Ética en el ejercicio de la labor docente universitaria. Revista de Filosofía, 39(Edición Especial Nº2), 312-324. https://doi.org/10.5281/zenodo.7302017

Vergara Castillo, A. B., Calderón, R. E., & Castrellón Calderón, X. (2021). EL CÓDIGO DE ÉTICA EN EL CONTROL DEL EJERCICIO DEL CONTADOR PÚBLICO AUTORIZADO. Revista FAECO Sapiens, 4(2), 43–61. https://revistas.up.ac.pa/index.php/faeco_sapiens/article/view/2177

Zeledón Ruiz, M. del P., & Aguilar Rojas, O. N. (2020). Ethics and university teaching. Perceptions and new challenges. Revista Digital de Investigación en Docencia Universitaria, 14(1), e1201. https://doi.org/10.19083/ridu.2020.1201

FINANCING

The authors did not receive funding for the development of this research.

DECLARATION OF CONFLICT OF INTEREST

The authors declare that there is no conflict of interest.

ACKNOWLEDGEMENTS

Thanks are extended to all the teachers who participated in the research.

STATEMENT ON THE USE OF ARTIFICIAL INTELLIGENCE

No artificial intelligence was used in the development of the article.

AUTHOR CONTRIBUTIONS

Conceptualization: Olga Calizaya Pari.

Data Curation: Nicohl Brenda Quispe Mamani.

Formal Analysis: Olga Calizaya Pari.

Investigation: Olga Calizaya Pari.

Methodology: Rafael Romero-Carazas.

Project Administration: Nicohl Brenda Quispe Mamani.

Software: Rafael Romero-Carazas.

Supervision: Rafael Romero-Carazas.

Validation: Nicohl Brenda Quispe Mamani.

Visualization: Nicohl Brenda Quispe Mamani.

Writing – Original Draft: Olga Calizaya Pari.

Writing – Review & Editing: Rafael Romero-Carazas.